What if the success of your kitchen expansion depends less on the marble you choose and more on the 2026 interest rate you secure today? You likely feel the weight of fluctuating market forecasts and the genuine fear of a "remodeling nightmare" where costs spiral out of control. It’s a common anxiety for homeowners in Fairfax and Loudoun County who want to upgrade their space without compromising their financial stability. Navigating the different types of home remodel loans can feel overwhelming when you’re trying to distinguish between a HELOC and a personal loan while economic indicators remain unpredictable.

This guide ensures you move forward with total confidence, helping you match the perfect financing structure to your specific Northern Virginia home transformation. We’ll explore how to secure fixed rates for predictable payments, align your loan disbursement with contractor milestones, and maximize your property’s ROI in the competitive NOVA real estate market. You’ll gain a clear roadmap to fund your vision while keeping your budget on track and your peace of mind intact.

Key Takeaways

- Discover why 2026 is a strategic year for Northern Virginia homeowners to invest and how to choose between flexible HELOCs and stable fixed-rate equity options.

- Explore specialized funding paths for major additions, such as financing Accessory Living Units (ALUs) or utilizing FHA 203(k) loans for historic Alexandria properties.

- Learn how to navigate the complex world of home remodel loans to secure the right financing that matches your specific property goals.

- Gain peace of mind by mastering budget planning, including how to calculate a vital 10-20% contingency fund for a stress-free renovation.

- Understand the “Elite Advantage” of the design-build model, which provides the fixed-price certainty lenders prefer and ensures your project stays on track.

Table of Contents

Understanding Home Remodel Loans in Northern Virginia

Home remodel loans are specialized financial tools designed to bridge the gap between your current living space and your vision for a dream home. Unlike general personal loans, these products are specifically structured for property enhancement, allowing you to invest in your asset’s long-term value. In 2026, Northern Virginia remains a powerhouse real estate market. Homeowners in McLean and Arlington are seeing record-high property values, which translates directly into increased borrowing power. This equity acts as a strategic lever, providing the capital needed to transform a dated house into a high-end masterpiece.

Choosing the right financing path is a critical first step. You’ll generally decide between secured and unsecured options. A secured home equity loan uses your property as collateral, which typically results in lower interest rates and higher borrowing limits. Unsecured renovation loans don’t require you to put your home on the line, but they often come with higher rates and shorter repayment terms. Selecting the best option depends on your project’s total scope and your personal comfort with debt structures.

Why Northern VA Homeowners Choose Remodel Loans

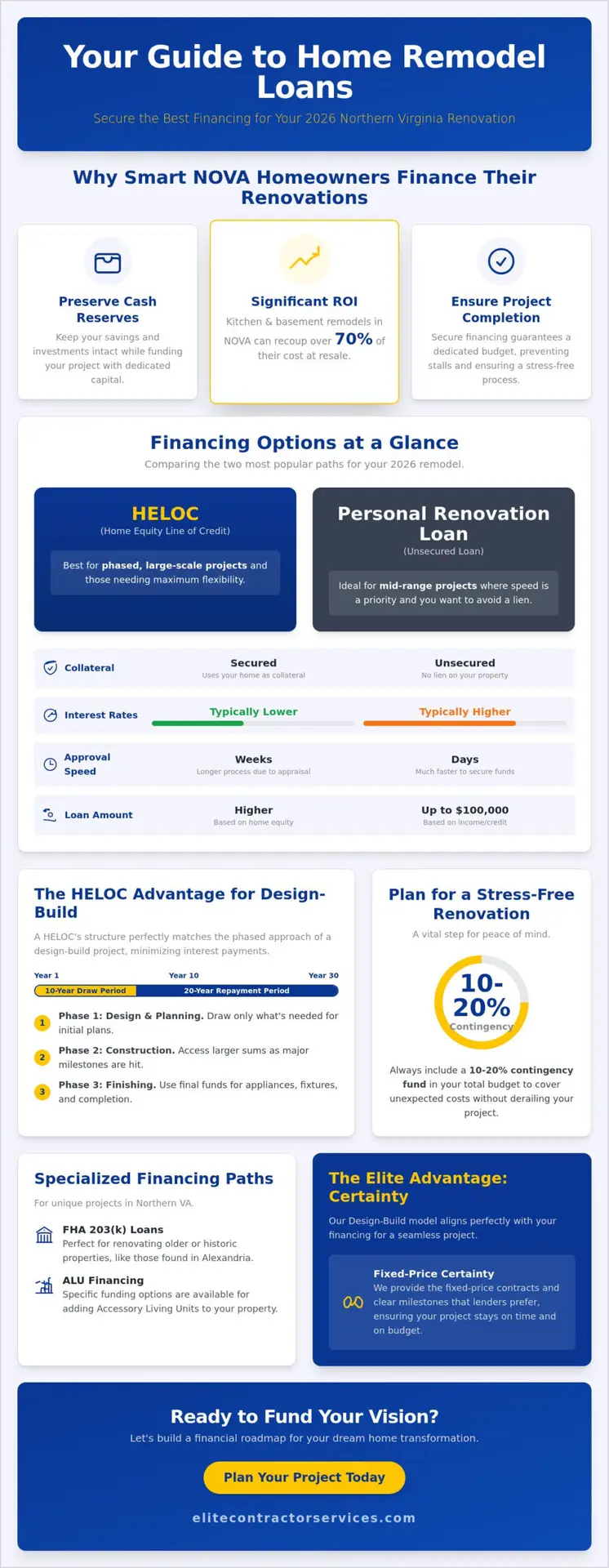

Smart homeowners in Fairfax County use home remodel loans to preserve their cash reserves for other investments while simultaneously improving their daily lifestyle. In this region, high-end kitchen and basement renovations often yield a significant return on investment, frequently recouping over 70 percent of costs upon resale. Proper financing also helps you avoid the "remodeling nightmare" of a project stalling mid-way. It ensures you have a dedicated budget to partner with a professional team that delivers a flawless, stress-free experience from start to finish.

The 2026 Interest Rate Landscape for NOVA

The 2026 market shows a stabilization of fixed interest rates, making them a popular choice for large-scale structural changes. While variable rates offer some flexibility for phased projects, the predictability of fixed payments is a major advantage for long-term planning. Northern Virginia’s consistent property appreciation has also improved the average Loan-to-Value (LTV) ratio for many residents. In Alexandria real estate, the LTV ratio is the specific percentage of your home’s current market value that is encumbered by your mortgage and other loans. A lower LTV ratio makes it much easier to secure the most competitive terms for home remodel loans.

Comparing Your Financing Options: Equity vs. Personal Loans

Selecting the right vehicle for home remodel loans in 2026 requires a clear look at your project’s timeline and your long-term financial goals. Northern Virginia homeowners often choose between leveraging their home’s built-up value or opting for the speed of unsecured funding. While equity-based options offer lower interest rates, they involve a longer approval process and put your property up as collateral. Personal loans provide a faster path to starting your renovation, though they typically carry higher rates and shorter repayment windows.

HELOCs: The Flexible Choice for Phased Design-Build

A Home Equity Line of Credit (HELOC) acts like a credit card secured by your home. It’s the most efficient tool for projects that happen in stages. Most HELOCs in 2026 feature a 10-year draw period followed by a 20-year repayment period. This structure allows you to take out only what you need, when you need it. You won’t pay interest on the full loan amount from day one; you only pay for the funds used to hit specific project milestones.

This flexibility aligns perfectly with the Elite Contractor Services three-step process. During the initial design and planning phases, your capital requirements are lower than during the heavy construction phase. By using a HELOC, you can manage cash flow meticulously as we move from conceptual drawings to the final build. This ensures you aren’t over-borrowing early in the project, which provides significant peace of mind as your vision comes to life.

Personal Renovation Loans: Speed Without Liens

If you want to start your Arlington kitchen refresh or basement upgrade within days rather than months, a personal loan is often the best fit. These loans are unsecured, meaning no lien is placed on your property. This removes the risk of foreclosure if your financial situation shifts. As of January 2026, lenders in the Northern VA market typically offer loan limits ranging from $3,000 to $100,000. These are ideal for mid-range projects that don’t require the massive capital of a full-scale addition.

To secure the most competitive 2026 rates in Fairfax or Loudoun County, you’ll generally need a credit score of 720 or higher. You can compare current market offerings through resources like the Forbes guide to the Best Home Improvement Loans to see how different lenders stack up. While the interest rates are higher than equity-based debt, the lack of closing costs and the rapid funding speed make them a favorite for homeowners who value agility.

It’s also vital to evaluate the tax implications of your debt. Under current 2026 tax guidelines, interest paid on home-secured debt is generally only deductible if the funds are used to "buy, build, or substantially improve" the home that secures the loan. Personal loan interest is not tax-deductible. Before you commit to a specific path for your home remodel loans, we recommend a quick chat with your tax professional to see which option maximizes your return on investment. If you’re ready to see how these numbers translate into a physical space, you can schedule a consultation with our team to discuss your project’s scope.

Specialized Financing for Major Northern VA Additions and ALUs

Major home transformations require more than just a standard credit line. Whether you’re adding an Accessory Living Unit (ALU) for a family member or expanding a footprint in Great Falls, the right home remodel loans provide the necessary capital without draining your personal savings. Since Fairfax County updated its ALU policies in 2024 to streamline approvals, these additions have become a popular way for homeowners to generate rental income or support multi-generational living. These projects are investments in property value that require a partner who understands the local zoning and financing landscape.

FHA Title I and 203(k) Options

Older homes in historic Alexandria or Arlington often lack the equity needed for a traditional HELOC. FHA 203(k) loans solve this problem by allowing you to borrow based on the home’s future value rather than its current appraisal. For cosmetic updates under $35,000, the Limited 203(k) is a fast, efficient option. However, structural changes like removing load-bearing walls or adding a full ALU require the Standard 203(k) path. To qualify, you must work with a HUD-approved consultant and a licensed contractor who can provide a detailed, line-item bid. This government-backed solution is ideal for "fixer-uppers" where the renovation cost exceeds 20% of the home’s current price.

Financing for High-End Home Additions

Elite projects in neighborhoods like Great Falls or McLean often exceed the limits of standard government-backed programs. When you’re planning a 1,500-square-foot second-story addition or a luxury sunroom expansion, a construction-to-permanent loan is often the most efficient path. This single-close loan covers the construction phase with interest-only payments, then converts to a traditional mortgage once the certificate of occupancy is issued. This prevents the stress of managing two separate closings and sets a predictable budget from day one.

Lenders for these high-limit home remodel loans rely heavily on an "As-Completed" appraisal during the approval process. This specific valuation calculates what your property will be worth after the elite-level upgrades are finished, rather than its current state. By using the projected future value, an "As-Completed" appraisal boosts your borrowing power and allows you to secure the funding required for complex structural expansions. Most "Elite" projects in Northern Virginia utilize this method to bridge the gap between current equity and the total project cost.

-

ALUs: Best for rental income or aging-in-place solutions.

-

FHA 203(k): Ideal for properties with limited current equity.

-

Construction-to-Permanent: Best for massive structural changes and high-limit budgets.

-

As-Completed Appraisals: Essential for maximizing loan amounts on luxury additions.

Planning Your Budget for a Northern Virginia Remodel

Setting a budget for a major renovation in Northern Virginia requires more than a ballpark figure. It’s about aligning your vision with financial reality long before the first hammer swings. By following a structured approach, you ensure your investment stays protected and your project remains on track through 2026 and beyond.

-

Step 1: Establish a realistic scope. Work with a design-build partner early in the process. This eliminates the common gap between an architect’s expensive blueprints and a contractor’s actual pricing, ensuring your project is buildable within your means.

-

Step 3: Calculate a contingency fund. Always set aside 10% to 20% of the total cost for unforeseen site conditions. In older Arlington or Alexandria neighborhoods, hidden issues like outdated 1950s wiring or foundation moisture aren’t rare and can quickly drain a tight budget.

-

Step 3: Evaluate resale value. Compare your project cost against current neighborhood data. A high-end renovation should reflect the ceiling price of homes in your specific Fairfax or Great Falls zip code to ensure a positive return on investment.

-

Step 4: Get pre-approved. Securing home remodel loans early provides a clear spending limit. It turns a stressful "what if" into a confident "let’s build," allowing you to lock in material orders before prices fluctuate.

Avoiding Budget Overruns in High-End Projects

Many homeowners fall into the trap of "cheap" estimates that lack granular detail. Our "Elite" contracts prevent such issues by providing an exhaustive scope of work that accounts for every fixture, finish, and structural requirement. This level of detail is why we recommend the design-build model. It allows us to lock in pricing before your loan closes, shielding you from the inflation spikes often seen in the luxury market. For a deeper look at how these costs break down, review our guide on Luxury Home Remodeling in Northern Virginia.

Local Cost Factors in Fairfax and Arlington

Northern Virginia has unique regulatory hurdles that impact your bottom line. Permitting fees in Fairfax County are based on project value and can add thousands to your initial estimates. Additionally, material lead times for custom cabinetry or high-end appliances can now reach 16 to 20 weeks. These delays don’t just slow down construction; they increase the interest-carry costs on home remodel loans. Our "Minimal Disruption" approach helps mitigate these indirect expenses. By maintaining a clean, organized job site, we often allow families to stay in their homes during construction, saving the $4,500 to $6,200 monthly cost of a short-term rental in Arlington.

Ready to build a budget that delivers peace of mind? Schedule your free estimate with our expert team today.

The Elite Advantage: Aligning Financing with Design-Build

Lenders view home remodel loans as exercises in risk management. In Northern Virginia’s competitive 2026 market, banks prioritize projects with predictable outcomes and fixed costs. The Design-Build model stands out because it offers a guaranteed price contract before a single hammer swings. This eliminates the budget creep common in traditional scenarios where architects and contractors work in silos. Elite Contractor Services bridges the gap between your financial approval and the physical build. We provide the precise data points your loan officer needs to greenlight the project with confidence.

Our team acts as a technical advocate through the estimation phase. We don’t just give you a number; we provide a roadmap. By integrating the design and construction phases, we ensure that the project you’ve financed is the project we deliver. This alignment is vital for maintaining the "on time and on budget" promise that has become our signature in the industry.

A Partnership Approach to Your Investment

Luxury lenders require more than just a rough estimate to approve high-balance home remodel loans. They demand a comprehensive package including architectural drawings, material specifications, and a line-item budget. We provide the detailed scope of work required by top-tier financial institutions to justify your home’s post-renovation appraisal. This meticulous planning ensures your project satisfies every loan term from the start. To understand why this integrated approach is the gold standard for 2026, explore why Top Design-Build Firms Near Me are the preferred choice for sophisticated homeowners.

Managing the draw process is often where remodeling projects stall. Banks release funds in stages based on verified progress. Elite Contractor Services coordinates directly with your lender’s inspectors to facilitate these payments. We handle the documentation and scheduling so your project never loses momentum due to administrative delays. This seamless coordination transforms loan administration into a routine, stress-free part of the project management cycle.

Starting Your Stress-Free Transformation Today

Preparing for a 2026 remodel requires early action and organized documentation. You’ll need tax returns, proof of equity, and a signed contract from a licensed, insured professional. Visiting a bank without a design-build partner often leads to lower loan valuations because the bank lacks a clear vision of the finished product. A professional consultation provides the concrete numbers necessary for a successful home remodel loans application. We help you align your aesthetic vision with your financing capacity from day one.

-

Collect your last two years of financial records and current mortgage statements.

-

Identify your primary renovation goals to help us build a targeted scope.

-

Consult with our team to create a project plan that maximizes your property value.

Don’t let the complexity of financing hold you back from your dream home. Our team is ready to guide you through every step of the process, from the first sketch to the final walkthrough. Schedule your free design-build estimate with Elite Contractor Services to begin your journey toward a stunning, flawlessly executed transformation.

Secure Your Northern Virginia Home Investment

Navigating the financial landscape of 2026 requires a clear strategy for your property. You’ve seen how choosing between equity-based options and personal home remodel loans can change your project’s trajectory. Whether you’re planning a high-end kitchen in Alexandria or an expansive addition in Arlington, the right funding is just the first step. Success in the Northern Virginia market depends on aligning your budget with a design-build partner who understands local regulations and the 2025-2026 permit requirements of Fairfax and Arlington counties.

Elite Contractor Services stands as a licensed and insured Northern Virginia general contractor, maintaining a reputation for excellence on platforms like Houzz and Angie’s List. We eliminate common remodeling nightmares by handling every phase from initial concept to the final walkthrough. You don’t have to manage multiple vendors or worry about hidden costs; we act as your dedicated partner to deliver results on time and on budget. Our expertise in high-end Alexandria and Arlington remodels ensures your home reflects the quality you expect.

Start Your Stress-Free Home Transformation with a Professional Estimate

Your dream home is within reach, and we’re excited to help you build it.

Frequently Asked Questions

How much can I borrow for a home remodel in Northern Virginia?

Borrowing limits depend on your chosen loan product and your property’s appraised value. For 2026, FHA 203(k) limits in high-cost areas like Fairfax County often reach $1,149,825 to accommodate local market demands. Most conventional lenders allow you to borrow up to 85% or 90% of your home’s post-improvement value. If your home’s future value is $900,000, you might access significant capital even if you’ve only lived there a short time.

Is interest on a home remodel loan tax-deductible in 2026?

Interest is generally deductible if you use the funds to substantially improve the home that secures the loan. According to current IRS guidelines, homeowners can deduct interest on up to $750,000 of qualified mortgage debt. You must itemize your deductions on your tax return to take advantage of this benefit. Since tax laws can shift, it’s vital to consult a professional tax advisor regarding your specific Arlington or Alexandria property.

Can I get a renovation loan if I have low equity in my home?

You can qualify for home remodel loans even with little equity by using programs that focus on the future value of your property. Fannie Mae HomeStyle and FHA 203(k) loans are designed for this exact scenario. Lenders look at what the home will be worth after our team completes your high-end addition or kitchen transformation. This option allows you to secure funding based on the 20% to 30% value increase your project creates.

What is the difference between a home equity loan and a HELOC for remodeling?

A home equity loan provides a single lump sum with a fixed interest rate, while a HELOC acts as a revolving line of credit. Home equity loans are ideal for large, one-time projects because they offer predictable monthly payments and a stable budget. HELOCs offer more flexibility if you plan to remodel in stages over several years. Most of our clients prefer the fixed loan to lock in costs for major structural changes.

How long does it take to get approved for a home improvement loan?

Approval timelines typically range from 30 to 45 days for secured financing like a HELOC or a construction-to-permanent loan. Unsecured personal loans move much faster, often reaching approval in 24 to 72 hours. The duration depends heavily on how quickly an appraiser can visit your home and verify the projected value. Having your financial documents and our detailed project scope ready will help us keep your renovation on a strict schedule.

Do I need a contractor estimate before applying for a remodel loan?

Most lenders require an itemized, professional bid before they’ll issue a final loan commitment. Banks need to see exactly how the money will be spent to ensure the project adds sufficient value to the property. We provide a comprehensive scope of work and a clear contract that meets these strict banking standards. This partnership ensures your financing covers the full cost of the transformation without any stressful mid-project budget shortfalls.

What credit score is needed for a high-end home addition loan?

Lenders generally look for a minimum credit score of 680 for most renovation products, but a score of 740 or higher unlocks the most competitive rates. High-end additions often require larger loan amounts, which means underwriters will scrutinize your debt-to-income ratio more closely. If your score is above 720, you’ll likely face fewer hurdles during the approval process. This financial strength helps ensure a smooth, professional experience from the first drawing to the final walkthrough.

Can I use a personal loan for a whole-house remodel in Arlington?

Personal loans are an option, but they’re often capped at $50,000 or $100,000, which rarely covers a full-scale renovation in Northern Virginia. In markets like Arlington, where high-end materials and specialized labor are standard, home remodel loans tied to your equity are usually more practical. These property-backed loans offer the higher limits and lower interest rates necessary for a flawless, full home remodel near me whole-house transformation. They provide the financial breathing room needed for elite results.